- Monthly Metals Mining Rundown - Free

- Posts

- Monthly Metals Mining Rundown for Month Ending 2 Apr 2026

Monthly Metals Mining Rundown for Month Ending 2 Apr 2026

Precious metals prices cratered during March by double digit percentage points, while lithium, copper, and nickel fell single digit percent - in a backdrop of broader equity markets falling ~5% during the month (ASX 200 fell -7.8%, S&P 500 and Nasdaq 100 both fell -5%, with MAG7 stock Microsoft MSFT now down -30% over past 3 months after closing March below its 200 week moving average for the first time in over a decade!); All of this led to most metal mining stocks also cratering by double digit percentage points or more, with losses led by precious metals miners falling by more than 20%; Includes covered announcements by HBM, AG, TUF, PAMPALO, USL, TCG, AUAU, OBM, DBG.

Host Rock Capital

April 04, 2026

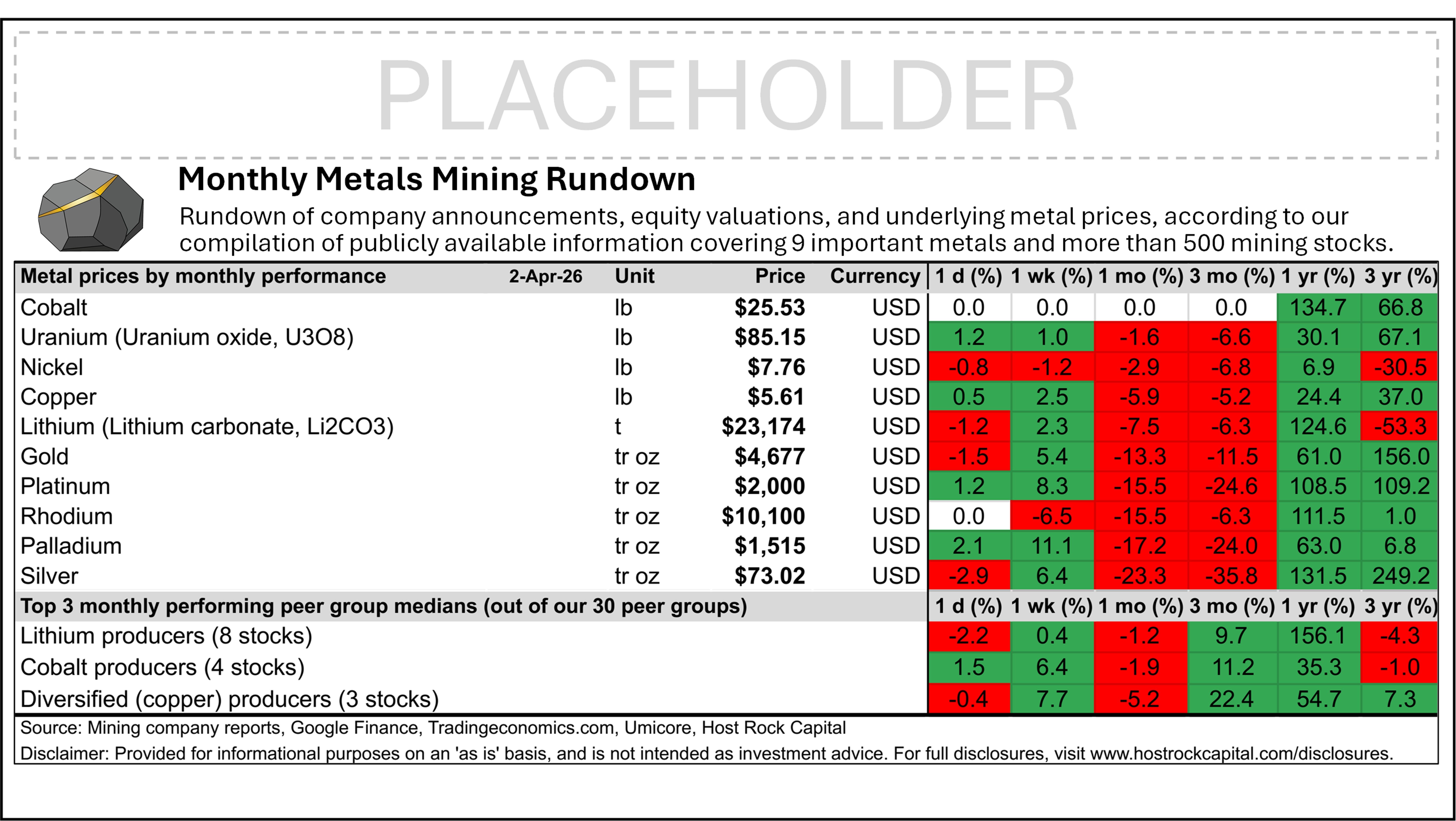

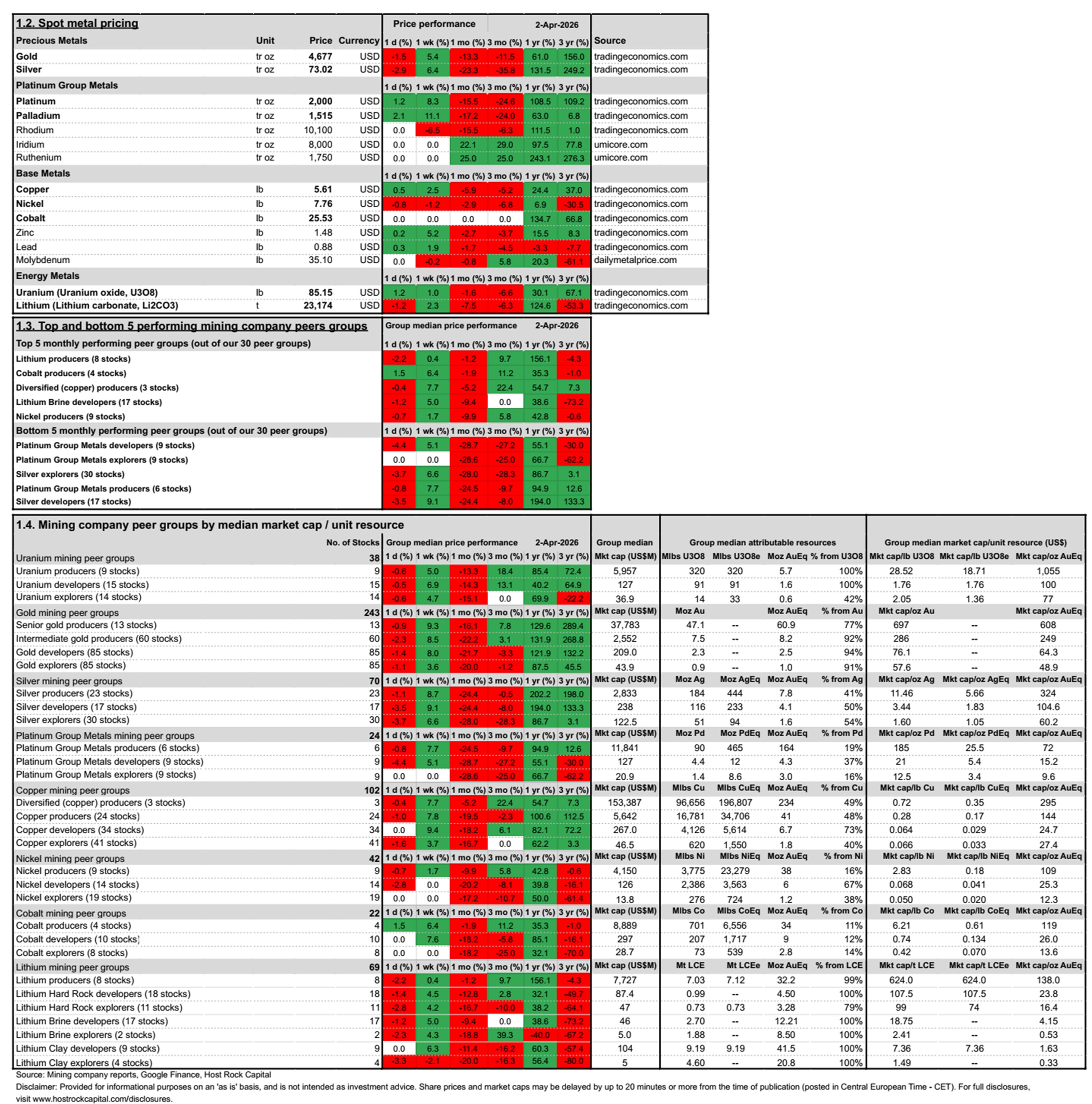

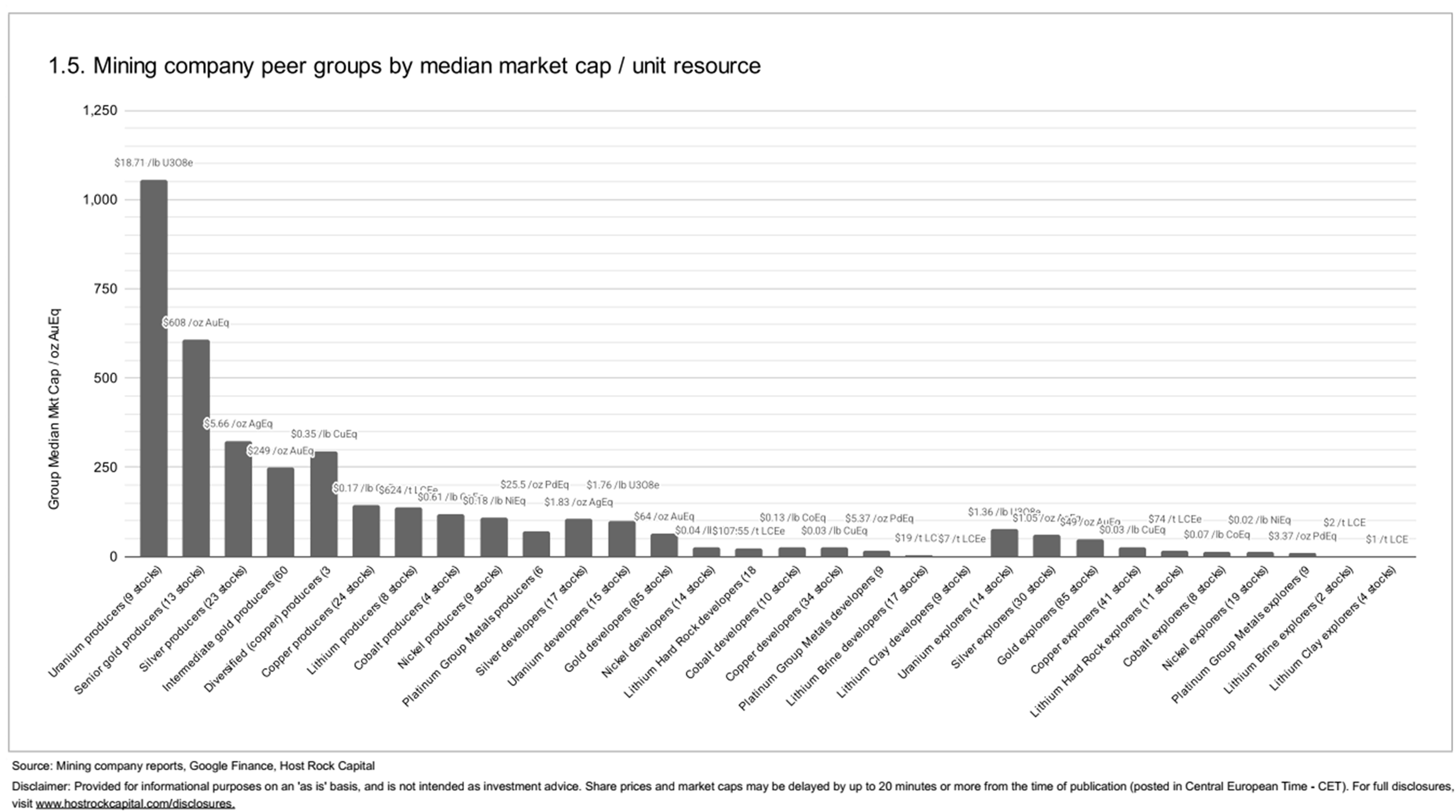

This past month’s metal price and top & bottom mining company peer group movers include:

2 Apr 2026

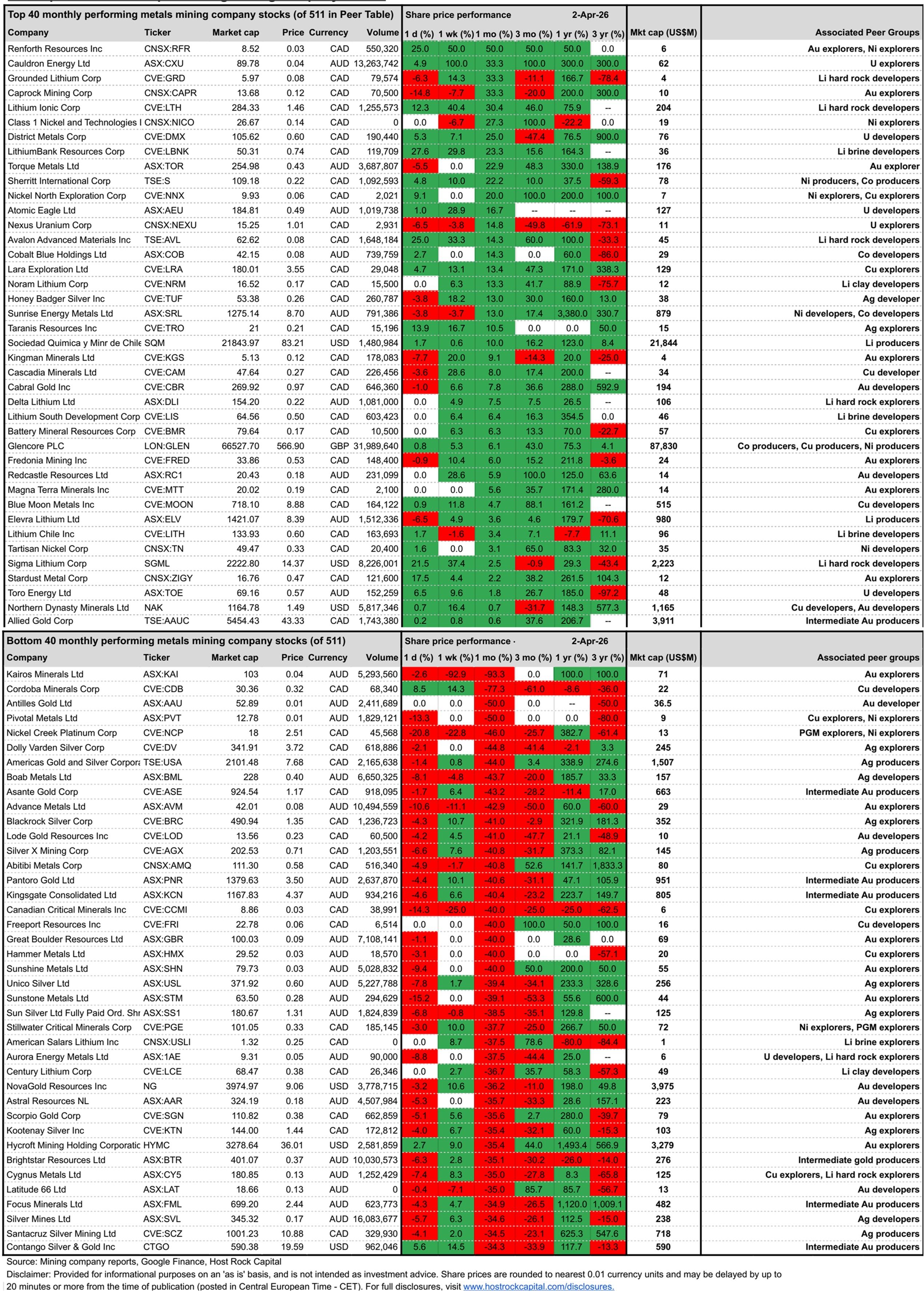

This past month’s top & bottom 40 performing metals mining stocks (out of Peer Table’s 511) include (share price rounding errors apply, as sourced from Google Finance):

Coverage of metals mining announcements incorporated into this month’s Peer Table (resource updates, economic studies, changes in attributable project ownership) include:

Copper producer Hudbay Minerals (NYSE/TSX:HBM) announced Friday (27 Mar) its annual reserves and resources update, which also included mine life extensions and improved production outlook. The announcement reaffirmed 2026 production guidance (of 110-138 kt Cu and 217-272 koz Au), and issued new production guidance figures for 2027 and 2028 – with 2027 guidance representing a +1-67% increase in copper production (140-184 kt Cu guided for 2027). According to our tallied numbers, HBM’s mineral resources now stand at 25.6 Blbs CuEq (35% from Cu, 36% from low-grade Mo, 22% from low-grade Au, rest Zn-Ag – at 3 month trailing average metal pricing with no recovery factors), but this excludes copper resources (of 12.7 Blbs Cu) from pending 100% acquisition of copper developer Arizona Sonoran Copper Company Inc. (ASCU:TSX) that hosts resources of 12.7 Blbs Cu (at Cactus project that’s near HBM’s existing Copper World project in Arizona), as recently announced March 2nd and due to close next quarter (Q2). The ASCU acquisition is set to grow HBM’s basic shares by ~11.5%. And including the 9.9% of ASCU that HBM already owns, HBM’s attributable resources of 26.9 Blbs CuEq (32.4 Moz AuEq) are set to grow by ~40% to 38.3 Blbs CuEq (56% from Cu, 24% Mo, 14% Au, rest Zn-Ag) on this acquisition. HBM stock is up +11% over past week ending 2 Apr (outperforming Cu producer median weekly gain of +8%), before closing the month ending 2 Apr down -19% to US$21.64/sh (in-line with Cu producer median monthly performance of -19.5%), proforma market cap US$9.6b (pending ASCU closing), and pro forma market cap/lb US$0.247/lb CuEq ($208/oz AuEq) (in between our 24-company Cu producer group median $0.17/lb CuEq/$144/oz AuEq and mean $0.254/lb CuEq/$213/oz AuEq) - and still a 29% discount to our diversified copper group median US$0.35/lb CuEq/$295/oz AuEq (although this is considered an upper bound valuation because substantial iron ore, aluminum and other non-metal resources are excluded from our diversified copper producer group).

2 Apr 2026

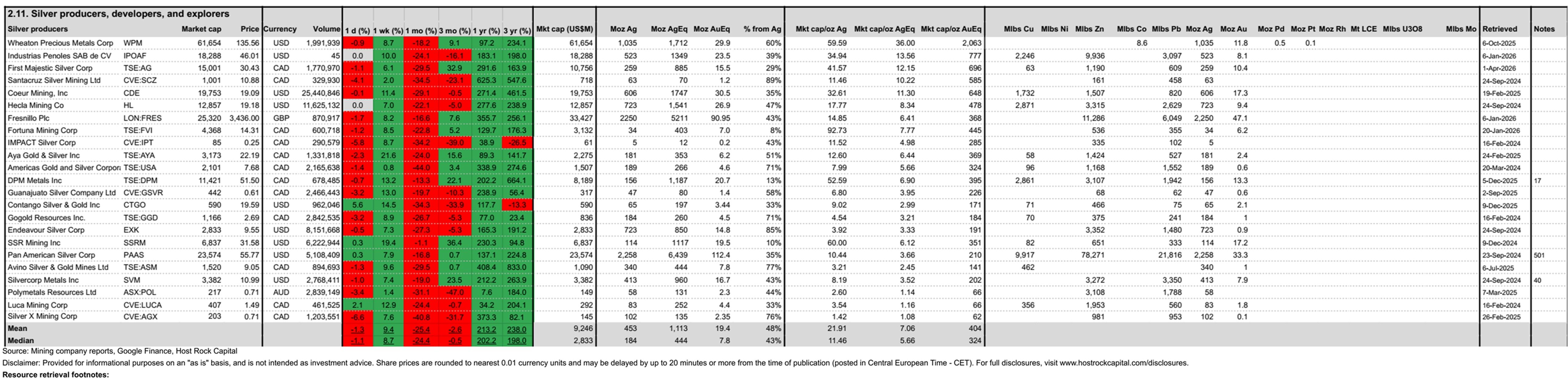

Silver producer and intermediate gold producer First Majestic Silver (TSX:AG) announced Tuesday (31 Mar) its annual reserves and resources update, which grew silver-equivalent reserves by +4% and Measured and Indicated silver-equivalent resources by a WHOPPING +69% - as reported by the company in the press release. Overall M&I&I resources also grew by roughly 50% according to our tally, to 885 Moz AgEq (15.5 Moz AuEq) at our estimated 3-month trailing average metal prices with no recovery factors – with a super high combined precious metals content of 96% (67% from Au, 29% from Ag, rest Zn-Pb-Cu). All of this helped AG stock rise +6% this past week (ending 2 Apr – outperforming both silver producer group median weekly performance of +16.5% and intermediate gold producer group median weekly performance of +14%), before closing the month (ending 2 Apr) down -29.5% at C$30.43/sh (slightly underperforming our silver producer group median monthly loss of -24.4% and int gold producer median -22%), market cap C$15b, and market cap/oz resource US$12.15/oz AgEq ($696/oz AuEq) – a premium valuation among most silver and intermediate gold peers on this metric (partly given its strong and fast-growing cash flow from its assets in Mexico that yielded Q4/25 silver-equivalent production of 8.9 Moz Ag - +56% year-over-year as reported by company on 15 Jan – based on the company’s reported updated 2025 guidance assumptions for metal prices), which led to 2025 cash flow from operations of US$526m (up 3.5-fold from 2024!). This makes AG one of the fastest growing silver and gold producers on the planet.

2 Apr 2026

2 Apr 2026

Former silver explorer – now silver developer (pending this transaction) – Honey Badger Silver Inc (TSX-V:TUF) announced intraday Thursday (19 Mar) the transformative acquisition of the Prairie Creek (“PC”) silver project in Canada’s Northwest Territories (NWT), from Resource Capital Fund VI LP (private equity), for consideration of C$10 million in cash plus C$2 million in TUF shares and warrants. PC is a major permitted silver-zinc-lead project located in NWT, with a historic (underground) resource estimate, economic studies including a 2021 PEA and a 2017 FS, and with an Impacts and Benefits Agreements (“IBA”) already signed with the two impacted indigenous governments. Project is accessible via winter road and significant investments have already been made towards an all-season road. Historic resources amount to 16.2Mt containing a reported 407 Moz AgEq (60% indicated) including indicated component of 9.8Mt @ 139 g/t Ag, 9.7% Zn, 8.8% Pb (766 g/t AgEq). These historically reported 407 Moz AgEq reduce to ~178 Moz AgEq at our Peer Table's estimated 3-month trailing average metal prices of $80.7/oz Ag, $1.48/lb Zn, and $0.91/lb Pb – which at these same prices are 42% from Ag, 40% from Zn, and 18% from Pb by metal value – and which MORE THAN TRIPLE the company’s mineral resource inventory to 261 Moz AgEq (now 43% from Ag, 41% Zn, and 14% Pb) when combined with TUF’s other resource stage projects (namely from Sunrise Lake also in NWT, and small starter resources at Clear Lake in Yukon and Yava in Nunavut). And based on the metal price sensitivity in the 2021 PEA from this new Prairie Creek project, a post-tax NPV8 of ~US$610 million was reported, at metal prices US$28.8/oz Ag and $1.44/lb Zn from initial capex of US$368m. TUF’s basic shares outstanding are set to grow by +58% to 205.3 m shares on this transaction (while more than TRIPLING resources to 261 Moz AgEq) after the C$2 million payment in shares and the associated C$10 million concurrent brokered private placement (led by SCP Resource Finance LP). TUF stock traded up +13% over past month ending 2 Apr (STRONGLY outperforming our silver developer group median LOSS of -24%) on the back of this major announcement, to 26c/sh (outperforming silver developer group median loss of -24% for same period), proforma market cap C$53m, proforma market cap/oz resource US$0.15/oz AgEq ($8.6/oz AuEq) - STILL a 92% discount to silver developer median $1.81/oz AgEq ($104/oz AuEq), and yielding a P/NAV (proforma market cap / post-tax NPV8 from 2021 PEA) of 0.063x at the study’s upper-bound metal prices ($28.8/oz Ag and 1.44/lb Zn, as mentioned above) – which is STILL a 94% discount to our 16-company silver developer group median 01.09x (at the same scaled-back silver price assumption of $28.8/oz Ag, for apples-to-apples comparison while not overstretching zinc price assumptions).

2 Apr 2026

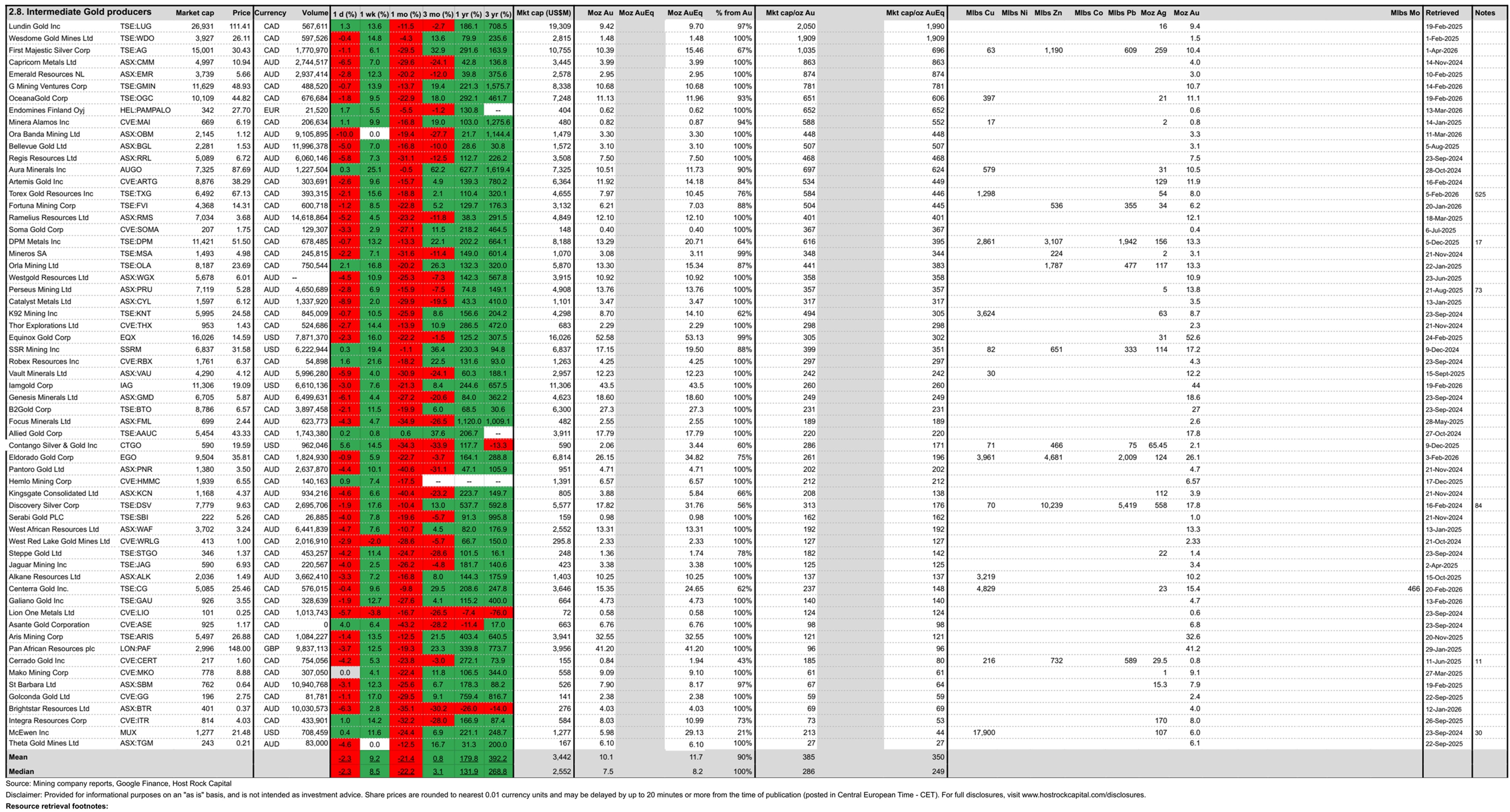

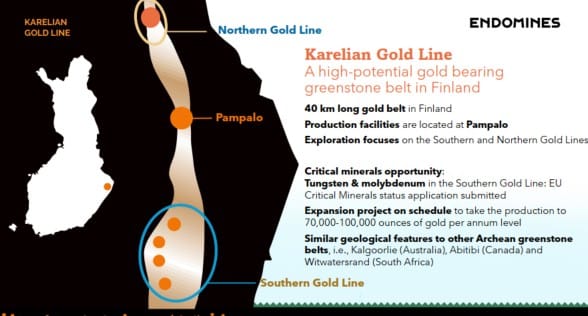

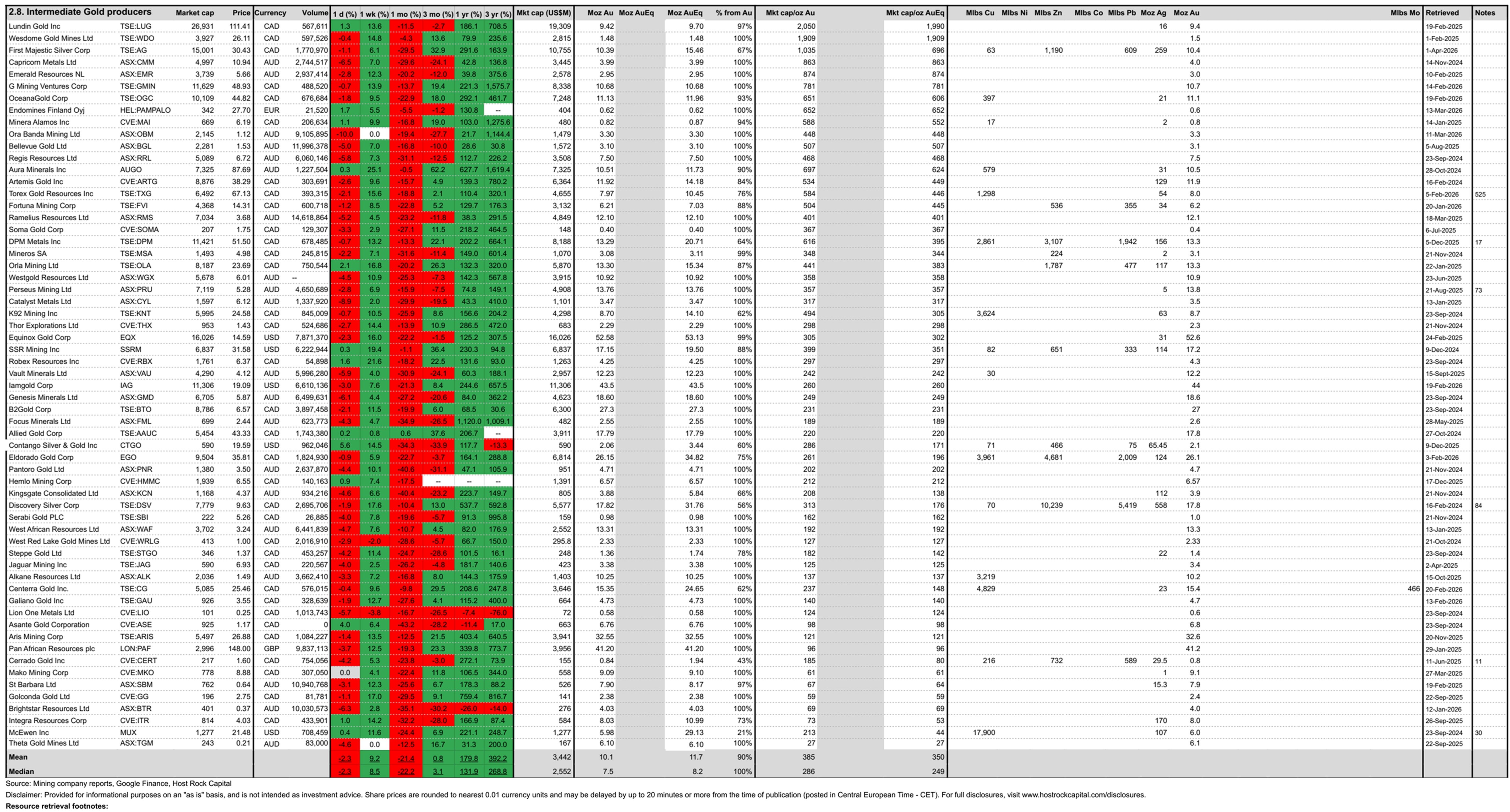

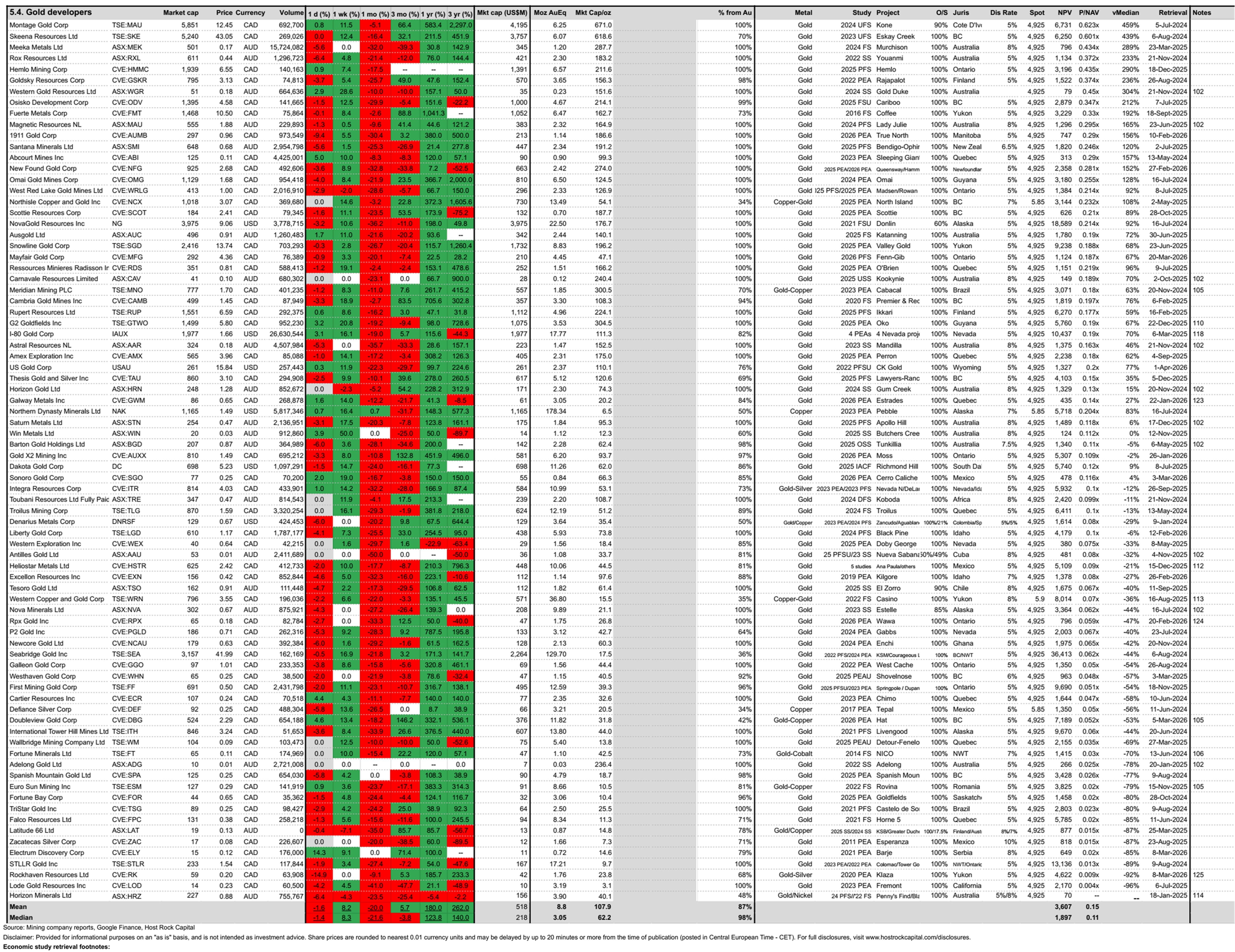

Intermediate gold producer Endomines (HEL:PAMPALO) announced Friday (13 Mar) updated estimates of reserves and resources that grew its overall Karelian Gold Line gold resources by +26% to 0.62Moz Au @ 1.85g/t Au within 11.66Mt, and grew reserve tonnage by +9.5% to 0.64Mt @ 2.29 g/t Au for 47.5koz (vs. ENDO’s 2025 production of 14.3 koz Au that was short of guidance of 16-22 koz). Endomines has come a long way in accumulating reserves and resources at its Pampalo mine and Karelian Gold Line trend since restarting its centrally located 0.45 mtpa Pampalo mill in December 2021 and (re)listing in Helsinki in Dec 2022 – and has not only replenished its production, but has also grown a multi-year runway of reserves as well as grown Karelian Gold Line resources close to management’s initially envisioned 1Moz target (that had appeared ambitious years ago) – helped by drilling success and a major new discovery (also announced last week on 10 Mar) of the Kartitsa (starter) deposit that accounts for 124koz of the company’s (620koz) resources. And the company is now targeting gold resources of 1.5-2Moz by 2030, with an aim to expand its mine and mill to allow for a multi-fold increase in gold production (targeting 70-100 koz per annum by 2030), according to company reports. Endomines stock dropped only +5.5% over past month ending 2 Apr (strongly outperforming our intermediate gold producer group median loss of -22%), to €27.70/sh, market cap €342m, and market cap/oz resource US$652/oz – a premium to group median US$249/oz AuEq, with the premium appearing attributable to Endomine’s decent 2025 cash flow from operations of €13.1m at starter production rate, relative to still relatively small/starter resources of ~0.6Moz (with multi-fold increases to these figures targeted for 2030).

2 Apr 2026

Silver explorer Unico Silver (ASX:USL) announced Tuesday (17 Mar) an updated resource estimate for its Joaquin deposit in Santa Cruz, Argentina – which grew its silver-equivalent ounces by +143% to 167 Moz AgEq, and which paves the way for an upcoming PFS for that project. Together with the company’s other nearby Cerro Leon project, combined mineral resources grew by ~44% to 266 Moz AgEq (4.5 Moz AuEq) based on our 3-month trailing average metal pricing, which are 69% attributable to silver, 24% from Au, rest Zn-Pb. USL stock gained +2.9% intraday 17 Mar, before closing the month ending 2 Apr down -39% to 60c/sh (underperforming our silver explorer group median monthly drop of -28%) , market cap A$374m, and market cap/oz resource US$0.97/oz AgEq ($56/oz AuEq) – a narrow premium to our 31-company silver explorer peer group median $1.05/oz AgEq ($60/oz AuEq), but a 47% discount to our 16-company silver developer peer group median US$1.83/oz AgEq ($105/oz AuEq) – where USL is headed soon.

2 Apr 2026

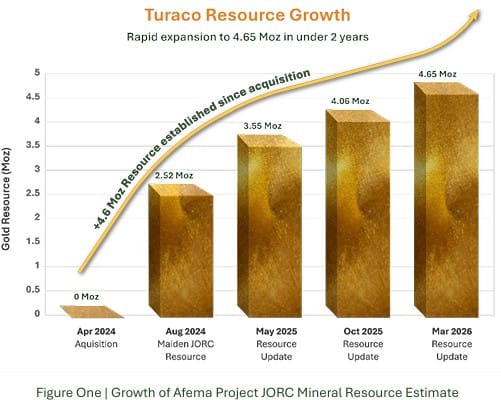

Gold explorer Turaco Gold (ASX:TCG) announced Wednesday (18 Mar) an updated mineral resource estimate (MRE) for its flagship Afema project in Cote d’Ivoire, West Africa, which incorporated additional drilling completed at the Woulo Woulo, Jonction, Anuiri, and Asupiri deposits, along with the brand new Herman deposit (next to Woulo Woulo). The MRE demonstrates continued/consistent growth since the maiden resource in 2024, with this next leg up adding +590koz (or +15%) bringing Afema project total to 4.65Moz within 115.3 Mt grading 1.3 g/t (98% pit constrained according to low/conservative gold price assumption of US$3,250/oz). TCG stock gained only +1% Wednesday (in-line with gold explorer median flat +0%), before closing the month ending 2 Apr down +21% to 63c/sh (in-line with group median weekly drop of -20%), market cap A$653m, and market cap/oz resource US$97/oz - in-line with group mean $96/oz and above median $49/oz - as TCG advances towards developer stage with a PFS and maiden ore reserve underway now, due for completion in Q2/26.

20 Mar 2026

Gold (and silver) explorer A2Gold (TSXV:AUAU) announced Friday (6 Mar) that it intends to acquire 100% interest in the Taylor gold-silver project in Nevada – the top ranked mining jurisdiction according to The Fraser Institute’s recent survcovered here: https://lnkd.in/ghivbYwX), where A2 is already advancing its flagship Eastside project on the state’s prolific Walker’s Lane trend. Eastside hosts low-grade resources of 1.4 Moz Au @ ~0.54g/t Au and 8.7Moz Ag @ 4.4 g/t Ag that are reported to be amenable to (low-capital-intensity) heap leach processing, and which excludes some 5-6 additional nearby target zones (along with some other early-stage projects A2 is advancing to the north - in Nevada’s Carlin trend near prolific Round Mountain mine). This new Taylor gold-silver project adds a second resource stage project to A2’s portfolio in Nevada, as it hosts historic resources of 11Moz Ag @ ~3g/t Ag (at high cut off grade associated with low silver price of US$17/oz Ag), which would at least double at a more current cut-off grade and silver price based on the cut-off grade sensitivity provided in the release – and which exclude extensive exploration upside, and A2 says drilling will at the project shortly after the acquisition is closed. Consideration is to include ~8.7m shares AUAU (valued at C$10m at 20-d VWAP), which will grow A2’s basic shares outstanding by ~8.3% to 112.39m shares, in exchange for growing its mineral resources by ~12.8% to 1.75 Moz AuEq (now a higher ~20% from Ag, 80% Au, by metal value at 3-month trailing average metal prices). AUAU stock traded down -12% over past month (ending 2 Apr) to 93c/sh – underperforming our 86-company gold explorer group median monthly drop of -20% for same period – and to a AUAU proforma market cap C$105m and proforma market cap/oz resource of US$43/oz AuEq – a 12% discount to gold explorer median $49/oz AuEq (and a 28% discount to silver explorer median $60/oz AuEq – whose median silver share of resources of 59% is much higher than AUAU’s 20%).

2 Apr 2026

Intermediate gold producer Ora Banda Mining (ASX:OBM) announced Wednesday an updated mineral resource estimate for its Round Dam multi-pit project in the Eastern Goldfields Province of Western Australia - which grew the deposit tenfold to 1.33Moz Au, and grew overall company-wide resources by +57% to 3.3Moz Au, with the majority (some ~2.8Moz) being co-located within ~40km of the Company’s operating 1.2Mtpa Davyhurst processing facility. This resource growth is from OBM’s ongoing A$73m (330km) 2026 exploration program, which continues to deliver outstanding results. OBM stock JUMPED +21.5% Wednesday following this news, before closing the month ending 2 Apr down -19% (just outperforming 62-company int gold producer group median weekly drop of -22%) to A$1.12/sh, market cap A$2.15b, and market cap/oz US$448 (was US$755/oz before this announcement) - which trades at a premium to group median US$249/oz AuEq (presumably due to strong cash flowing gold production, with OBM’s cash flow from operations doubling in H2/25 to A$102 million), and is a 26% discount to senior gold producer group median $608/oz AuEq (the group that could acquire this portfolio when the time is right).

2 Apr 2026

Former gold and copper (and cobalt) explorer – now developer – Doubleview Gold Corp (TSXV:DBG) announced Monday (2 Mar) a maiden PEA for its flagship Hat project in the Northwestern reaches of Canada’s western-most frontier of British Columbia. The study’s base case (A1 scenario) yielded a post-tax NPV of C$4.96b at consensus metal pricing of $3,272.60/oz Au and $4.88/lb Cu, from initial capital of C$3.55b. And this NPV: (a) increases to C$11b at spot metal pricing US$5,200/oz Au and $6.00/lb Cu, (b) assumes conservative metal recoveries of 66% for Au and 80% for Cu according to past test work, which are expected to be improved to 75% for Au and 89% for Cu (increasing the NPV to C$6.7b at consensus metal pricing or C$13.5b at spot prices, as shown under the PEA’s A2 scenario), (c) excludes a possible scandium circuit (which the PEA shows improves the NPV marginally under scenario B). DBG stock dropped -7% (in-line with Cu developer median -8%) over week (ending 6 mar), before closing month (ending 2 Apr) down -16% (outperforming gold developer monthly drop of -22% and Cu developer group median monthly drop of -18%) to C$2.29/sh or market cap C$524m, with Hat’s large resource base of 11.9Moz AuEq or 9.9 Blbs CuEq (50% Au, 42% Cu, 6% from Co, rest Ag - excluding Hat’s Scandium resources) trading at a market cap/oz resource of US$32/oz AuEq ($0.038/lb CuEq) for a 50% discount to gold developer group median $64/oz AuEq. And according to the separate metal price sensitivities provided in the PEA for Cu and Au (for the conservative A1 scenario), DBG now (4 Mar) trades at a P/NAV (market cap/NPV) of 0.052x at 3-month trailing average metal pricing of US$4,925/oz Au and $5.85/lb Cu – a 53% discount to our gold developer group median 0.15x at same $4,925/oz Au and a 28% discount to our copper developer group median 0.07x at same $5.85/lb Cu.

2 Apr 2026

2 Apr 2026

Copper producer Hudbay Minerals Inc. Minerals (NYSE:HBM) announced Monday (2 Mar) the acquisition of copper developer Arizona Sonoran Copper Company Inc. (ASCU:TSX | ASCUF:OTCQX) and its large pure-play copper Cactus project in Arizona, which hosts resources of 12.7 Blbs Cu, and has a 2025 PFS that yields a post-tax NPV of US$4.36b at our estimated 3-month trailing average copper price of $5.85/lb – translating to a (2 Apr) ASCU P/NAV (market cap/NPV) of 0.24x AFTER ASCU stock gained +11% over the week ending 2 Apr (in betwee with 34-company copper developer group mean 0.25x and above median 0.07x at same copper price). And importantly, this acquisition will create the third largest copper district in North America together with Hudbay’s existing Copper World project (also in Arizona), with expected annual copper production of 92,000 t Cu (203 Mlbs Cu) from 2030 – some time after which Cactus is now due to add another 103,000 t Cu per annum (227 Mlbs Cu). Together with HBM’s other near-term optimization projects, this deal provides HBM with a clear pathway to more than double its overall copper production from ~125,000 t Cu per annum now (275 Mlbs Cu) to over 250,000 t Cu annually (551 Mlbs Cu) by 2030 from Copper World, and ultimately to 350,000 t Cu per annum (771 Mlbs Cu) from Cactus (~2.8x HBM’s current Cu production levels). HBM will issue 0.242 sh HBM per share ASCU in all-stock deal, valued at C$9.35/sh ASCU for 30% premium to prior close and 36% premium based on both HBM and ASCU’s 20-day VWAP. HBM’s basic shares will increase by ~11.5% to ~442.3m to acquire the remaining 90.1% of ASCU shares outstanding (HBM already owned 9.9%), to grow its mineral resource inventory by ~14% to 95.8 Blbs CuEq (115.6 Moz AuEq) – 66% from Cu, 24% from Au, 7% from Ag, rest Zn (by increasing HBM’s attributable ownership of ASCU’s resources from 9.9% to 100%). HBM’s stock dropped -19% over past month ending 2 Apr trading days (in-line with our 24-company copper producer median drop of -19.5% for same period) to US$21.64/sh, proforma market cap US$9.6b (pending ASCU closing), and pro forma market cap/lb US$0.224/lb CuEq ($208/AuEq) (in between our 24-company Cu producer group median $0.17/lb CuEq/$144/oz AuEq and mean $0.254/lb CuEq/$213/oz AuEq) - and still a 29% discount to our diversified copper group median US$0.35/lb CuEq/$295/oz AuEq (although this is considered an upper bound valuation because substantial iron ore, aluminum and other non-metal resources are excluded from our diversified copper producer group).

2 Apr 2026

28 Feb 2026 - Gold developer Sonoro Gold Corp (TSXV:SGO) announced the results of an independent updated mineral resource estimate (MRE) and an updated PEA on its flagship Cerro Caliche gold project in Sonoro, Mexico. The study contemplated a 10-yr, 16 ktpd open pit and heap leach operation. Mineral resources increased by 73% to 0.83 Moz AuEq (85% Au/15% Ag) according to our retrieved numbers, which helped increase production rates compared to the 2023 PEA. And although this 2026 study’s somewhat larger mine plan with higher production rates did not quite offset cost inflation since the 2023 study (NPV fell slightly by ~5% at our recent 3-month trailing gold price $4,747/oz), this MRE and PEA was reported to reflect less than 30% of the known mineralized zones on the Cerro Caliche concession that was recently nearly tripled in size - so the potential for future expansion of the proposed mine in both capacity and mine life is considered high (as management reports). Post-tax NPV is US$478m at our estimated 3-month trailing average gold price $4,925/oz Au, and yields a similar P/NAV of 0.12x at 27c/sh (in-line with 77-company gold developer group median 0.11x at same $4,925/oz Au) - after SGO stock dropped -17% over past month ending 2 Apr (outperforming group median drop of -21.5%), to 25c/sh, market cap C$77m, market cap/oz resource US$66/oz AuEq (in-line with group median US$64/oz). The study’s reported post-tax NPV was US$224m at gold price US$3,500/oz from initial capital of only US$83m including $11m contingency (heap leach does not require a costly mill) with fairly low AISC of US$1,902/oz (mid-range AISC seems to have risen in recent years from the ball park of ~US$1,500/oz to ~$2,000/oz - reflecting reference gold prices of $3,000/oz and $4,000/oz according to the rule of thumb that AISC should be one-half of the gold price in the long term).

2 Apr 2026

Disclaimer: Provided for informational and educational purposes on an ‘as-is’ basis, and is not investment advice. For full disclosures, visit www.hostrockcapital.com/disclosures.