- Monthly Metals Mining Rundown - Free

- Posts

- Monthly Metals Mining Rundown for Month Ending 27 Feb 2026

Monthly Metals Mining Rundown for Month Ending 27 Feb 2026

Precious metals prices SURGED during February (after experiencing sharp downward corrections in late January from record highs), with silver rising +11%, gold rising +8%, and platinum rising +12% - all 3 of which are reapproaching recent all-time high territories from late January; Other metal prices gained more gently, except the uranium price which fell -13%; Large-cap silver and gold stocks dominated the miners - mostly rising 10-20% or more, with mining stocks for most other metals rising more gently during the month, except small-cap Li mining stocks which mostly fell slightly (while Li producers mostly gained +6.5% or more) and except for U mining stocks which mostly fell -5% or more; Includes covered announcements by NFG, EVNI, GCU, DBG, SIG, LCE, EXN, BTR, AUE, CG, SBM, RPX, LUN, IAG, AIS, PEX, AUMB, AMQ, FRES, PRB, EGO, PUR.

Host Rock Capital

March 01, 2026

This past month’s metal price and top & bottom mining company peer group movers include:

27 Feb 2026

This past month’s top & bottom 40 performing metals mining stocks (out of Peer Table’s 504) include (share price rounding errors apply, as sourced from Google Finance):

Coverage of metals mining announcements incorporated into this month’s Peer Table (resource updates, economic studies, changes in attributable project ownership) include:

Gold developer (and small-scale producer) New Found Gold Corp. (TSXV:NFG) announced Thursday (26 Feb) a PEA and slightly enlarged resource for its Hammerdown mine in Newfoundland, which just had its first gold pour in Nov. 2025 with production currently ramping up towards commercial levels the company expects to reach by yearend. The study replaces the old 2022 Feasibility study, and ought to better reflect current mine plan and operations. Including the (unchanged) 2025 PEA for NFG’s much larger Queensway development project, NFG’s combined post-tax NPV5 at our 3-month trailing average gold price of US$4,747/oz fell just a hair to US$2.27b from this study, which yields a P/NAV 0.42x (at C$3.79/sh on 27 Feb) after stock rose +1.6% over past month ending 27 Feb (underperforming gold developer median +11%), which is just above the upper-quartile-range or 75-percentile range of our gold developer peer group with median 0.15x and mean 0.20x. And this P/NAV (market cap/NPV) should rise as production continues to ramp up – perhaps to the ~1x range once commercial production is reached (although most of this NAV or NPV is from non-producing development project Queensway, so perhaps a P/NAV of 0.6-8x is a more likely interim target).

27 Feb 2026

Nickel developer EV Nickel Inc. (TSXV : EVNI) announced on 26 Feb a maiden resource estimate for the Gemini North nickel zone at its large Carlang nickel project in Ontario outside of Timmins, which grew the project’s overall metal-equivalent resources by ~9% to 6.57 Blbs NiEq (10.6Moz AuEq) – 88% from Ni. EVNI stock rose gently following this news, and is up +4.5% over past month ending 27 Feb (outperforming 14-company nickel developer group mean monthly loss of -4.5%) to C$0.23/sh (27 Feb), market cap C$32m, market cap/lb resource US$0.004/lb NiEq ($2.24/oz AuEq) – a 93.5% discount to group median US$0.056/lb NiEq ($35/oz AuEq) and a 47% discount to other (even) large(r) (similarly) low-grade Ni peer in the Timmins camp - Canada Nickel Company TSXV:CNC which trades at market cap/lb US$0.007/lb NIEq (4.36/oz AuEq). And Carlang also has a 2025 PEA, which yields an P/NAV for EVNI of 0.019x at the bottom of our Ni developer peer group (at our reference Ni price of US$9.50/lb) – a 90% discount to group median 0.19x, and a still-wide 87% discount to peer CNC’s 0.15x at same Ni price.

27 Feb 2026

Copper developer Gunnison Copper (TSX: GCU | OTC: GCUMF) announced Wednesday (27 Feb) an updated PEA for its Gunnison project in Arizona, which supersedes the prior 2024 PEA, and incorporates operational enhancements including addition of high-grade Strong & Harris satellite deposit, material sorting, cement and limestone co-products, and optimization, with average annual production of 174 Mlbs Cu in first 15 years of mine life. These improvements more than offset any cost inflation over the past 1-2 years since the 2024 study, and actually increased the post-tax NPV8 by just over 12% at both our (newly increased) reference copper price US$4.50/lb and our 3-month trailing average Cu price $5.73/lb, leading to P/NAV (market cap/post-tax NPV8 from this study) of 0.10x and 0.06x at both prices respectively – for 46% and 42% discounts to our 34-company copper developer group medians 0.19x and 0.10x, respectively. And this is after GCU stock already rose +3.4% on back of this news over past month ending 27 Feb (in-line with copper developer median performance +4%), to C$0.60/sh and market cap C$254m. The reported post-tax NPV8 at US$4.60/lb Cu was US$1.95b from initial capital of US$1.54b (including contingency) with low all-in-sustaining cash costs of US$2.06/lb Cu.

27 Feb 2026

Gold, copper, and cobalt explorer Doubleview Gold Corp (TSXV:DBG) announced Wednesday (25 Feb) a substantial resource update for its flagship Hat project, in the northwest of Canada’s western-most frontier of British Columbia, which grew gold-equivalent resources by ~64% to 11.96Moz Au at our estimated 3-month trailing average metal prices with no metal recovery factors (50% Au, 42% Cu, 6% Co, 2% Ag), from a reported 609Mt indicated @ 0.21% Cu, 0.18 g/t Au, 0.008% Co and 0.4 g/t Ag (for a reported 0.43% CuEq) and 503Mt inferred @ 0.18% Cu, 0.19 g/t Au, 0.008% Co, and 0.4 g/t Ag (for a reported 0.41% CuEq), which includes a higher-grade central core grading over 0.50% CuEq. And all this excludes additional mineral resources of Scandium Oxide of 4.4 kt Sc2O3 (indicated + inferred). This ~64% increase in resources helped DBG stock MORE THAN DOUBLE over past month ending 27 Feb, to C$2.68/sh, market cap C$604m, and market cap/oz resource US$37/oz AuEq ($0.045/lb CuEq) – which is STILL a 41% discount to our 84-company gold explorer median US$63/oz AuEq (and in-line with 38-company copper explorer group median US$0.044/lb CuEq or $37/oz AuEq).

27 Feb 2026

Gold explorer Sitka Gold Corp (TSXV:SIG) announced Wednesday (25 Feb) a significant resource update for its flagship RC Gold project in Canada’s northwestern-most frontier of Yukon. The update added a large maiden inferred resource for the Rhosgobel Gold project amounting to 2.25Moz Au @ 0.70 g/t Au – which includes a higher-grade core at surface grading >1g/t to help boost initial cash flows in prospective future operation, and grew the Eiger gold deposit to 0.535Moz Au @ 0.52 g/t. Along with the project’s main Blackjack deposit that was updated last year, this announcement roughly DOUBLES Sitka’s indicated + inferred resources to 5.12 Moz Au, which investors have started to appreciate as they pushed SIG stock up +26% over past month ending 27 Feb (outperforming gold explorer group mean monthly gain of +9%) to C$1.11/sh, market cap C$413m, and market cap/oz resource now roughly halved from this announcement to US$59/oz Au (now a 6% discount to gold explorer group median $63/oz).

Lithium clay developer Century Lithium Corp (TSXV:LCE) announced Monday (23 Feb) an updated Feasibility Study for its large flagship Angel Island lithium project in Nevada (formerly Clayton Valley in 2024 FS) which optimized its flowsheet that relies on Direct Lithium Extraction technology – which the jury is still on out among the investment community and for which there are no existing large-scale operations, but for which LCE has validated through a reported four years of pilot plant operations in Nevada. After-tax NPV8% was improved to $4b at Li price assumption $24,000/t Li carb from initial capex of $997m for initial 7,500 tpd options (expands to 15,000 tpd later for another $660m). LCE stock gained +7% over past month ending 27 Feb (outperforming Li clay developer median loss of -3%) to C$0.61/sh, market cap C$101m, market cap/t Li carb US$11.1/t ($3/oz AuEq), and P/NAV 0.02x at our estimated at our estimated 3-month trailing average Li price US$19,519/t LCE – in-line with our 9-company Li clay developer group median 0.02x (as same Li price).

27 Feb 2026

Gold (and silver-lead-zinc) developer Excellon Resources Inc. (TSXV:EXN) announced Monday (23 Feb) a substantial resource update for its past-producing Mallay Silver-Lead-Zinc mine in Peru, that grew indicated silver resources 6-fold, and amounted to 0.89Mt indicated @ 195 g/t Ag, 3.33% Pb, 4.83% Zn and 0.36Mt inferred @ 149 g/t Ag, 2.67% Pb, 4.32% Zn. The project also has a 600 tpd mill that was first commissioned in 2012, and this MRE establishes a higher-confidence inventory to underpin a staged restart plan – while new upside targets are also advanced. But this resource is peanuts in size compared to its other Kilgore project in Idaho, that hosts resources of 0.96 Moz Au and has a 2019, which today’s announced update for Mallay increases to 1.08 Moz AuEq at our estimated 3-month trailing average metal prices. But investors seemed to like the existing mine and mill restart potential associated with this Mallay resource update, and EXN stock rose +32% over past month ending 27 Feb on this news (outperforming gold developer peer group median gain of +12% for same period) to C$0.66/sh, market cap C$226m, and market cap/oz resource US$153/oz AuEq (premium to gold developer median and mean $89 and $144/oz AuEq), but on P/NAV based on 2019 PEA for Kilgore gold project (which completely excludes this past-producing Mallay mine with restart potential) EXN trades at 0.32x at our reference gold price of US$2,500/oz – a 31% discount to our 77-company gold developer peer group median 0.46x (at same gold price).

27 Feb 2026

Gold explorer Bonterra Resources Inc. (TSXV:BTR) reported yesterday (23 Feb) updated mineral resources estimates for its Barry and Gladiator deposits in Quebec, which grew contained M&I resource ounces by 30% and inferred by 21% compared to 2021 estimate. Gold Fields (JSE:GFI) is earning-in up to 70% of the project according to the encompassing Phoenix JV, from a C$5m payment (paid) and C$30m in expenditures over 3 years. BTR stock has traded up +11% over past month ending 27 Feb (outperforming peer group mean +3.5%), to C$0.20/sh and market cap C$43m. And BTR’s proforma 30% of today’s announced resource estimate (1.03 Moz) trades at market cap/oz resource US$30/oz – a 52% discount to our 85-company gold explorer peer group median $63/oz AuEq.

27 Feb 2026

Gold explorer Aurum Resources (ASX:AUE) announced today (23 Feb) an updated mineral resource estimate (MRE) for its Boundiali gold project in Cote d’Ivoire - reported to be a major milestone for the project that grew its indicated resources by +49% or +450koz to 1.37Moz Au, making it a premier large-scale West African gold asset and paves the way for an upcoming PFS. This reported higher confidence resource growth brings total project resources to 3.03Moz and company resources to 3.90 Moz (up +19%) - including 0.87Moz from Napie gold project which also has an MRE update in the pipeline for delivery this quarter. AUE stock gained +17% this past month ending 27 Feb on back of this news (outperforming group median monthly performance of +3.5%) to 76c/sh, market cap A$271m, market cap/oz resource US$49/oz - a 22% discount to our 85-company gold explorer group median US$63/oz.

Copper producer and intermediate gold producer Centerra Gold (TSX:CG) announced Thursday (19 Feb) its annual reserves and resources update that grew gold and copper reserves by a reported +58% and +49% to 5.5Moz Au and 3.56 Blbs Cu, with overall resources rising roughly 10% to 24.9 Moz AuEq (62% from Au, 24% from Cu, rest Ag-Mo) - demonstrating excellent year-over-year replacement of both reserves and resources. CG stock gained +1.4% (in-line with intermediate gold producer median +1.6%) Thursday following this news, before closing the month (ending 27 Feb) up +26% (outperforming both our Cu producer group median performance of +7% and our intermediate gold producer group median +14%) to C$28.67/sh, market cap C$5.7b, and market cap/oz resource US$169/oz AuEq - a 52% discount to intermediate gold producer median $350/oz AuEq (and in-line with Cu producer median US$0.21/lb CuEq or $171/oz AuEq)

27 Feb 2026

Intermediate gold producer St. Barbara (ASX:SBM) announced on 20 Feb its annual reserves and resources update, which grew resources by +14% or 1Moz to 7.9Moz, with reserves remaining relatively unchanged at 3.8Moz (was 4.0Moz). And a small share of silver resources and reserves (15.3 Moz and 4.5 Moz) are now also reported from Simberi operations in Papua New Guinea. SBM stock traded flat +0% on the day of this news, before closing the month (ending 27 Feb) up +14% to A$0.83/sh, market cap A$1.0b, and market cap/oz resource US$88/oz - for a wide 74% discount to our 60-company intermediate gold producer median US$350/oz AuEq.

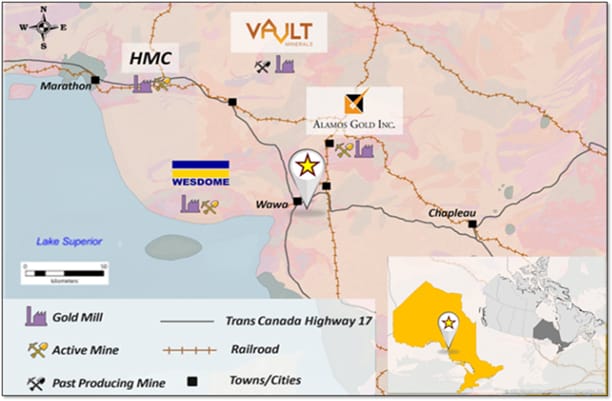

Former gold explorer - now gold developer - RPX Gold (TSXV:RPX) announced Wednesday (18 Feb) a toll-milling PEA for its 100%-owned Wawa gold project in Northwestern Ontario, Canada, with project resources of 1.75 Moz Au. The study outlined a phased development plan beginning with open pit mining followed by underground mining, and assumed material will be crushed and transported by highway truck to an off-site toll milling facility for processing in the region (although no toll milling arrangement has been negotiated or agreed upon yet). Post-tax NPV C$523 from initial capex of C$51m, with AISC US$2,149/oz. RPX stock traded down somewhat following this news - closing the month ending 27 Feb up +18% ( outperforming our 82-company gold developer peer group median monthly performance +12%) - as investors may have questioned the value of this toll-milling PEA with no arrangement in place at a time when most mills ought to be a full capacity due to high gold price. Share price was (on 27 Feb) C$0.26/sh, market cap C$93m, market cap/oz resource US$39/oz AuEq - a 60% discount to our gold developer group median US$89/oz AuEq (although most developers have on-site mills), and a 56% discount to our 85-company gold explorer group median US$60/oz AuEq.

27 Feb 2026

Copper producer Lundin Mining (TSX:LUN) announced Wednesday (18 Feb) its annual reserves and resources update that grew M&I copper resources by +37% on 100%-ownership basis (+17% on attributable basis), overshadowing a 42% drop in copper reserves (because the now larger M&I resource should ultimately be converted into reserves). And a significant share of these resources are non-cash-flowing from development project Filo del Sol within its broader Vicuña project 50% held by LUN in a JV with BHP - for which a possible looming construction decision could re-rate their market value. LUN’s overall attributable resources grew to 142 Mlbs CuEq (173.5 Moz AuEq) at our 3-month trailing average metal prices (55% from Cu, 35% from Au, 10% from Ag), which helped LUN stock gain +3.6% on 18 Feb after this news (vs. copper producer peer group median performance of flat +0%), before closing the month (ending 27 Feb) up +27% to C$43.46/sh (strongly outperforming peer group median gain of +7.3%), market cap C$37b, and market cap/lb resource US$0.19/lb CuEq ($157/oz AuEq) - still a 8% discount to our 24-company copper producer group median US$0.21/lb CuEq ($171/oz AuEq).

27 Feb 2026

Intermediate gold producer Iamgold (NYSE:IAG) announced on 17 Feb its annual reserves and resources update, that saw a +22% jump in M&I resource tonnage to 1.0 Bt and a +16% increase in contained gold ounces to 31Moz Au, overshadowing a slight -7% drop in reserve gold ounces to 9.9Moz. Overall combined M&I + inferred resources grew to 43.5Moz Au, and IAG stock traded roughly flat on this news, and finished the month (ending 27 Feb) up +35% (more than double group median monthly gain of +15%) to US$24.57/sh, market cap US$14.55b, and market cap/oz resource US$334/oz Au - STILL a narrow 5% discount to our 60-company intermediate gold producer median US$350/oz AuEq, and a much wider 54% discount to the more advanced senior gold producer group median US$729/oz AuEq (the group that could acquire IAG for its solid portfolio of multiple producing mines in the great low-risk mining jurisdiction of Canada).

27 Feb 2026

Copper producer Aeris Resources Limited Resources (ASX:AIS) announced Thursday (12 Feb) the acquisition of the South Cobar copper project from copper (and silver) explorer Peel Mining Limited (ASX:PEX), in an arrangement where AIS acquires all outstanding shares of PEX for its main copper asset (South Cobar with MRE 10.64Mt @ 1.85% Cu, 18 g/t Ag, 0.22 g/t Au, 0.10% Zn, 0.12% Pb) according to a share exchange ratio of 0.3363 sh AIS per share PEX valued at 19c/sh (16% premium to recent share price 16c/sh), and where PEX shareholders retain full ownership of its remaining precious and base metals assets in the Cobar Basin by way of new ASX listing/spin-out (valued at an additional 20c/sh PEX, increasing the combined equity premium for PEX shareholders to 49% at recent VWAP) – including the high-grade zinc-polymetallic Southern Nights complex (MRE of 10Mt @ 7.69% ZnEq) and the May Day deposit (1.6Mt @ 0.98g/t Au, 25 g/t Ag, 0.92% Zn, 0.61% Pb) as mentioned in the news release, but also appearing to include the South Cobar zinc-dominant deposit for an additional (significant) 10.66Mt @ 2.87% Zn, 0.42 g/t Au, 52 g/t Ag, 0.36% Cu, 1.34% Pb. The deal increases AIS’ basic shares by ~25% to 1.506b to grow its copper resources by ~25% (and copper-equivalent resources by ~15%) to 4.5 Blbs CuEq (5.6 Moz AuEq) – now (a larger) 48% from Cu (was 44%), 26% Au, 12% Ag, rest Zn-Pb at 3-month trailing average metal pricing with no recovery factors. The added project comes with 2 large high-grade copper deposits within trucking distance of AIS’ producing Tritton mine complex with its 1.8 mtpa processing plant – pushing out the mine's life to 10+ years, and creating a platform for further consolidation in the Cobar Region. Copper price is up ~40% in the past year, including ~20% in the last few months, while AIS is ramping up production (guiding for 24-29 kt Cu in 2026 – up from 19 kt in 2025) with a now enlarged resource base. AIS stock dropped -6% on 12 Feb after this announcement (vs. Cu producer group mean daily drop of -2.7%), before closing the month (ending 27 Feb) down -14.5% to A$0.51/sh (strongly underperforming copper producer median monthly gain of +7% - with the majority of the drop in AIS share price happening BEFORE the deal was announced) to proforma market cap A$798m or US$0.124/lb CuEq resource ($103/oz AuEq) – a 40% discount to 24-company Cu producer median US$0.206/lb CuEq ($171/oz AuEq) and a 70% discount to our 60-company intermediate gold producer median US$350/oz AuEq.

(2/2) And the deal looks even sweeter with even more upside for PEX shareholders – via the proposed NewCo junior miner (Peel Mining Limited "NewCo"), which effectively swaps ~30% of its pre-existing 2.38Moz mineral resource inventory (31% Cu, 29% Ag, 17% Au, rest Zn-Pb) for 20.5% equity ownership share of AIS’ proforma 4.5 Blbs CuEq (5.6 Moz AuEq) while retaining ownership of PEX’s other assets, which actually GROWS PEX (NewCo) attributable mineral resources by 18% (compared to former PEX) to 2.80 Moz AuEq (174 Moz AuEq) – which is now quite silver-dominant with 26% of its metal value coming from Ag, 25% Au, 26% Cu, 20% Zn, res Pb – and 𝘄𝗵𝗶𝗰𝗵 𝗴𝗿𝗮𝗱𝘂𝗮𝘁𝗲𝘀 𝗣𝗲𝗲𝗹 𝗠𝗶𝗻𝗶𝗻𝗴 𝗡𝗲𝘄𝗖𝗼 𝘁𝗼 𝗼𝘂𝗿 𝟯𝟬-𝗰𝗼𝗺𝗽𝗮𝗻𝘆 𝘀𝗶𝗹𝘃𝗲𝗿 𝗲𝘅𝗽𝗹𝗼𝗿𝗲𝗿 𝗽𝗲𝗲𝗿 𝗴𝗿𝗼𝘂𝗽 (PEX had been considered a copper-dominant copper explorer previously, but the silver explorer group enjoys a higher market cap/oz peer group median that is ~2.5x higher than Cu explorer group on metal-equivalent basis). The proposed ASX listing/spin-co effectively acts as a 4.6-to-1 share consolidation where PEX shareholders will receive 1 share NewCo valued at 4.4c/sh NewCo (~20c/sh PEX) for every 4.6 shares PEX (reducing PEX basic shares from 917m to 199.4m NewCo shares), and was announced to be combined with a A$4m Initial Public Offering (IPO) at 20c/sh NewCo (equivalent to 4.4c/sh PEX) – which will increase Peel Mining NewCo shares by ~10% to 219.4m. PEX stock traded up +12.5% on 12 Feb, before closing the month (ending 27 Feb) up +6% to $0.18/sh, proforma (NewCo) market cap A$39m, or market cap/oz US$0.17/oz AgEq ($10/oz AuEq) – an 86% discount to our 30-company silver explorer group median $1.30/oz AgEq ($76/oz AuEq) – and a 73% discount to (former) PEX’s recent/pre-deal (copper-dominant) market cap/oz resource of US$38/oz AuEq.

27 Feb 2026

27 Feb 2026

Former gold explorer – now gold developer – 1911 Gold Corporation (TSXV:AUMB) announced Tuesday (10 Feb) a PEA for its True North gold project in Manitoba – which historically produced ~2Moz from 10Mt @ 7g/t with recoveries of 94% at rates up to 2,250 tpd from a process plant that is still in-place. The PEA contemplates an UG mine producing 4Mt @ 4.32 g/t Au over 11-yr LOM at rate of 1,215 tpd with high gold recovery 93.5%, yielding a post-tax NPV5 of C$391m from pre-production capital of only C$109.9m (largely given existing mill) with decent AISC of US$1,897oz, which jumps to a NPV5 of $998m at recent spot gold $4,800/oz. And this True North past-producing mine is surrounded by numerous past-producing mines within trucking distance to True North mine, which could be used to expand production in the future – especially given this PEA only uses some ~54% of the True North mill’s historical maximum mill capacity of 2,250tpd. AUMB stock surprisingly dropped on this news (and it appeared to be shorted by bad actors) and traded on strong volume down -10% the week ending 13 Feb (underperforming group median gain of +2%), before closing the month ending 27 Feb UP +13% (in-line with group median monthly gain +12%) to C$1.22/sh, market cap C$375m, and P/NAV (market cap/NPV) of 0.38x at our 3-month trailing average gold price US$4,747/oz – roughly around the upper-quartile-range or 75-percentile of our 76-company gold developer peer group (that has a median 0.15x and mean 0.20x at same gold price). But AUMB stands out because it has an already-built/permitted mill, and is therefore is already fairly de-risked and well on its way to production targeted in 2027 after a PFS that is being kicked off in H2/2026. Once commercial production is reached, this P/NAV should approach the ~1x range (from current ~0.33x range) – pending results of future studies including PFS as this PEA is preliminary in nature.

27 Feb 2026

Copper explorer Abitibi Metals Corp (CSE:AMQ) announced Thursday (5 Feb) an updated resource estimate for its flagship B26 polymetallic project in Quebec, of which it owns 50% with an option to earn an additional 30% for 80%.

The update incorporated 42.98km of drilling completed in 2024/25, and grew attributable resources by ~70% (since 2024) to 1.16 Blbs CuEq (80% ownership basis) – which are 54% from Cu, 25% from Au, 14% Ag, rest Zn – at our 3-month trailing average metal pricing with no recovery factors.

The reported tonnage and grades for the underground resource estimate were (100% basis):

• Indicated: 12.96Mt @ 1.19% Cu, 1.16% Zn, 0.44 g/t Au, 30.8 g/t Ag, 0.05% Zn, 0.01% Pb (2.08% CuEq or 2.81 g/t AuEq)

• Inferred: 12.34 @ 1.60% Cu, 0.16% Zn, 0.68 g/t Au, 8.1 g/t Ag, 0.01% Pb (2.20% CuEq or 2.97 g/t AuEq)

And this deposit should continue to grow, including from another 40km of drilling that is already underway as part of the 2026 program.

AMQ stock gained on the news, and is up +12% over the past week (ending 6 Feb, intraday) – strongly outperforming our 39-company Cu explorer median weekly loss of -3.3%.

AMQ stock gained +6.5% on Friday alone (6 Feb), before closing the month ending 17 Feb up +22% (outperforming peer group median monthly gain of nil +0) to 89c/sh, market cap C$167m, and market cap/lb resource US$0.104/lb CuEq ($86/oz AuEq) assuming 80% ownership of project resources – just below the upper-quartile-range (75-percentile) of our 39-company Cu explorer peer group, and just above the mean US$0.082/lb CuEq ($68/oz AuEq) and well above median US$0.044/lb CuEq ($37/oz AuEq). And these group average market cap/lb valuations appearing rather low, as many Toronto listed junior copper mining stocks continue to appear shorted by bad actors.

27 Feb 2026

Silver producer and senior gold producer FRESNILLO PLC (LON:FRES) announced a few weeks ago (on 22 Jan) the completion of its acquisition of gold developer Probe Gold Inc. (TSX:PRB) and its ~8Moz flagship Novador project in Quebec which includes 4 past-producing mines, along with additional resources of some ~2Moz split across a few other project areas (also in Quebec). The all-cash deal was first announced a few months ago (on 31 Oct 2025), and was valued at C$3.65/share PRB or ~C$780m (US$560m), for a 24% premium to PRB’s 30-day VWAP (on 30 Oct 2025). Fresnillo is one of the world’s largest primary silver producers and a major Mexican gold producer, with a portfolio of 8 key operating mines in Mexico plus exploration/development properties, and this deal marks the company’s (welcomed) slight diversification into Canada/Quebec 🤝🫡 . FRES adds 10Moz of resources for a price of US$56/oz (and P/NAV of 0.13x from 2024 PEA at recent spot gold $4,441/oz – in-line with gold developer median 0.13x at same gold price) - increasing FRES’s resource inventory by ~13% to 88.2Moz AuEq (now 41% from Ag and 53% from Au for a huge 94% from precious metals, rest Pb-Zn byproduct), traded (on 27 Feb) at a FRES market cap/oz resource of US$471/oz AuEq ($8.00/oz AgEq) – a 35% discount to 13-company senior gold producer group median US$729/oz AuEq, and a 49% discount to fellow silver dominant peer Coeur Mining, Inc. NYSE:CDE $928/oz AuEq ($15.8/oz AgEq) and an 81% discount to the top silver dominant peer Wheaton Precious Metals NYSE:WPM US$2,525/oz AuEq ($42.9/oz AgEq) – AFTER FRES stock gained ~70% over past ~3 months since closing this deal (more than the performance of the senior gold group median of +50% for exact same period - suggesting FRES investors liked the deal).

27 Feb 2026

27 Feb 2026

Intermediate gold (and copper & silver) producer Eldorado Gold (NYSE:EGO) announced Monday (2 Feb) the acquisition of copper developer Foran Mining (TSX:FOM) and its flagship 100%-owned McIlvenna Bay project in Saskatchewan which is under construction with commercial production due mid-2026. FOM shareholders will receive 0.1128 shares EGO (and US$0.01/sh) per share FOM in a mostly all-share deal worth C$3.8b - an 8% premium to the 20-day VWAP and nil premium to closing price on 30 Jan (after FOM gained +35% during Jan – outperforming our 35-company copper developer peer group median monthly gain of +17%). Eldorado already had 4 producing mines across Canada, Greece and Turkiye – and now adds the McIlvenna Bay 4,900 tpd UG mine with resources of 39 Mt @ 2.02% CuEq (indicated) and 5Mt @ 1.8% CuEq (inferred) – and also a pipeline of other similar projects including Bigstone with a starter 4.4Mt resource and Tesla with an exploration target 28-45Mt grading 0.9-1.3% Cu. EGO’s pre-existing resources of 31.71 Moz AuEq (81% from Au, 10% from Cu, rest Pb-Ag) now become slightly diversified with FOM’s C-Zn dominant resources (growing on this deal by ~10% to 35.0 Moz AuEq, still a dominant ~75% from Au). FOM’s resources of 2.6 Blbs CuEq (48% from Cu, 22% from Zn, rest Ag-Pb-Au) had traded at the very top of our Cu developer peer group at market cap/lb of US$0.90/lb CuEq ($728/oz AuEq) and P/NAV of 3.9x at 3-month trailing average Cu price $5.50/lb. The valuable premium may be partly justified by FOM’s deep pipeline of projects, and might also be slightly overhyped on its near-term production status. The high valuation makes deal a win for FOM shareholders. It’s also a win for the gold sector (as it TAKES THE PUCK from the copper sector with this acquisition/absorption of this poster child asset). The scarcity value of the near-term cash flows from Cu (whose price has risen ~+40% over past year) and especially from Zn (whose price has risen ~21% over past year to US$1.50/lb, and for which there are few to no primary Zn mines that can be ramped up to plug widening supply shortages). EGO’s basic shares outstanding will rise ~24% to ~265m. Investors traded EGO stock up +8% (over past month ending 27 Feb - underperforming int gold producer median gain +15%) to US$46.42/sh, market cap C$12.3b, and market cap/oz US$259/oz AuEq – a 26% discount to the int. gold producer group median US$350/oz AuEg (giving FOM shareholders renewed upside). And although the drop in EGO share price raises the question/possibility that its shareholders might not approve this deal, continued rising of the copper and ZINC prices in the near term on widening supply deficits could ease any concerns EGO shareholders have on FOM’s valuation, and help push the deal over the line.

27 Feb 2026

Former lithium brine explorer – now developer – Pursuit Minerals Ltd (ASX:PUR) announced on 2 Feb results of a PFS and maiden reserve for its flagship, 100%-owned Rio Grande Sur project in Salta Province, Argentina. The study contemplates 5,000 tpa for 25-yr mine life from 6 production wells and a network of evaporation ponds, yielding a post-tax NPV8 of US$364m from initial capital of US$136.5m at a LT Li price of $27,500/t Li carbonate (that the study assumes is variable, starting at US$15,714/t Li carb first year, and rising to $22,500/t Li carb by year 4, and finally to $27,500/t Li carb from year 6) - with low all-in sustaining costs US$6,520/t. PUR stock inched higher following this news, before closing month ending 27 Feb flat +0% over past month (ending 27 Feb) - underperforming our 16-company Li brine developer peer group median monthly gain of +7.6% - to A$0.12/sh PUR (27 Feb) and market cap A$26m, market cap/oz resource US$14.6/t LCE (27% discount to group median US$20.2/t LCE) and P/NAV of 0.10x at our 3-month trailing average Li price US$19,519/t LCE (in-line with Li brine developer median 0.08x).

27 Feb 2026

Disclaimer: Provided for informational and educational purposes on an ‘as-is’ basis, and is not investment advice. For full disclosures, visit www.hostrockcapital.com/disclosures.